Nukes in neglect

A five bagger in boring old utilities?

“When the facts change, I change my mind. What do you do, sir?”

— John Maynard Keynes

Utilities are regulated, highly leveraged, capital intensive and rate-base driven, so various investing metrics do not map cleanly to the same in other industries. Many investors just ignore them as bond proxies. But I’ve had an interest in them for a while. If you wait for the right opportunity, there’s money to be made even in a boring old utility.

Are Utilities just bond proxies?

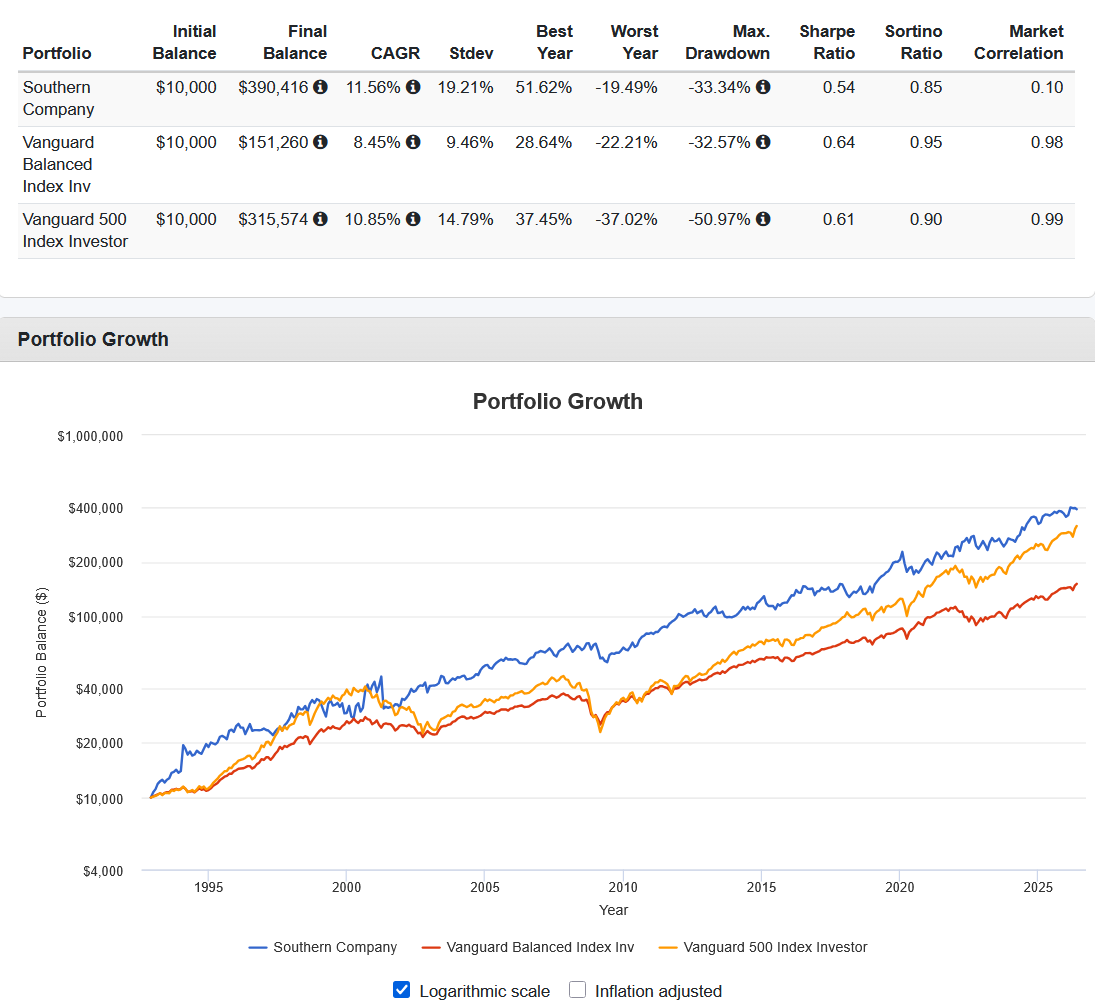

Here’s an interesting question. Since the first Vanguard Balanced Index fund (60% equities/40% bonds) became available in Dec 1992, which would have given you better returns? The Balanced fund, S&P 500 or a boring old utility?

As you can see the answer is a utility, Southern Company. Surprised?

Utilities might have become a bit more interesting of late, but the answer does not change if you stopped the analysis before ChatGPT’s launch and the subsequent AI driven power demand. Of course, it was helped by the period having two major bear markets where being perceived as a bond proxy would have helped. But then we also had COVID, inflation and rising rates which would have detracted from that benefit. I'm not saying go ahead and invest only in utilities, but rather the point is that you should not ignore them. They have a place in a portfolio.

Some practitioners like DFA maintain that utility stocks with regulated returns do not earn enough, but is that really true? As a group in an index that might be true, but you need to be selective and pick the right utility stocks.

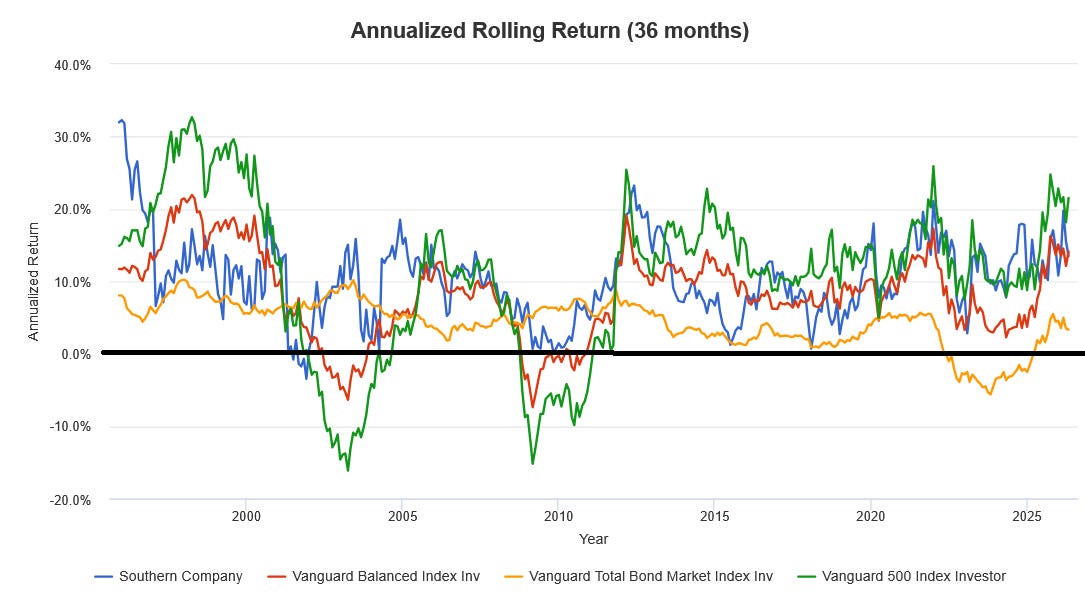

They can be less risky as well. See the 3-year rolling returns below. Rarely dipped below zero for long. That cannot be said for even balanced funds and bonds!

What I find strange is that academic research calls for blending uncorrelated less risky assets with risky ones, yet that seems to be ignored within stock portfolios (other than minimum volatility portfolios) and typically utilities are thrown out. But there is at least one professional investor who understands and uses utilities masterfully in a balanced fund to almost keep up with the S&P 500. David Giroux of T. Rowe Price who runs $PRWCX which is possibly the best balanced fund of all time. As Morningstar says -

“… their execution of the strategy has been consistently excellent. Compared with competitors, the portfolio typically leans more heavily on technology, healthcare, and utilities. The utilities may seem out of place, but they provide defensive balance when markets turn volatile.”

Over the years he has written more than once about the potential of utilities.

Nuclear antipathy

I’ve had the opportunity to visit a nuclear power plant twice. Once as part of my dad’s (unrelated) work and once as part of a school competition. Naturally, you get exposure to how nuclear power is a force for good etc.

But after the Fukushima nuclear accident in 2011, the world’s reaction was essentially that of irrational politically toxic tail risk - “If one reactor can fail, all nuclear must go”. I used to be more pro-nuclear power before Fukushima, but it exposed some tail risks that the industry didn’t talk much about before and I became more circumspect. However, the subsequent reaction by the world was literally cutting off your nose to spite your face.

For example, Germany immediately shut down eight reactors with a full phaseout despite nuclear previously supplying 25% of their needs. This was predominantly replaced with higher polluting coal and many excess deaths attributed to it. They also sleepwalked into a dependency on Russian natural gas, barely managing to avoid an energy crisis due to the war in Ukraine. Smaller versions of this played out in Japan and a few other European nations. The Uranium and nuclear supply chains were also hit with extreme pessimism and depressed prices under the assumption that nuclear would never come back.

Broken markets and pariah assets

Although the US did not shutdown as many reactors, the market did not fare much better although the specific drivers were different. Natural gas plants were making it very difficult for existing nuclear plants to survive.

Nuclear power plants have high fixed costs and low fuel costs. Think amortization/financing of expensive bespoke construction, highly trained staff, security, inspections/compliance, insurance etc. In comparison, in the mid 2010s, gas plants were cheaper to construct, interest rates were cheap post GFC and there was excess capacity. A nuclear plant is typically designed for always on baseload power and cannot run less or shutdown. Gas plants could run only when needed and when profitable.

The utility industry has a unique structure due to its regulated monopoly nature and can be quite complicated to analyze with many different parties trying different policies to improve or “fix” things. In the large PJM Interconnection market, the design was broken in that the marginal supply set the price for electricity instead of also accounting for the long duration reliability and base load capability of nuclear power. The market-clearing price was not designed to recover everyone’s full cost every hour. It priced existing nuclear like a commodity, until later problems and scarcity revealed that existing nuclear was an insurance against many of the same problems.

Exelon’s plan to jettison nuclear assets

Nuclear power did have other issues like high construction costs, but I changed my mind and decided that this had gone too far. The pendulum had to swing back. After all these were already built, low carbon, high-capacity factor and fuel secure electricity assets. Some were running after Uranium miners and physical nuclear fuel ETFs etc., but due to my interest in utilities I decided to poke around those with a high exposure to nuclear plants.

I came across the utility Exelon EXC 0.00%↑, whose generation arm was the largest operator of nuclear power plants in the United States and the largest non-governmental operator of nuclear power plants in the world.

Not long after this, in Feb 2021, Exelon announced a plan to spin off its generation arm as Exelon Generation (SpinCo) and keep all the regulated utilities as Exelon Utilities (RemainCo) a pure regulated transmission and distribution utility.

“If you hear about a spinoff, or if you’re sent a few fractions of shares in some newly created company, begin an immediate investigation into buying more.”

— Peter Lynch | One Up on Wall Street

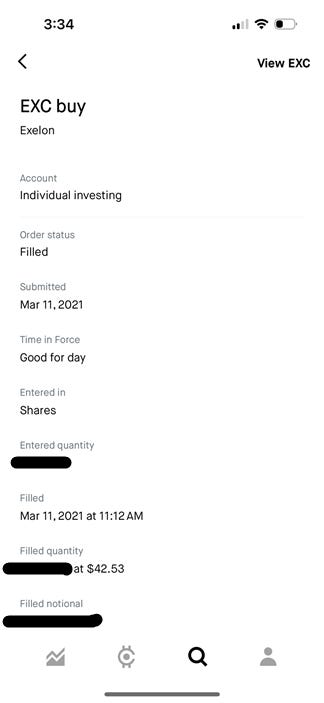

I investigated it a bit and it seemed like most of the plan was to try and market the nuclear plants as “green” to get state credits and retire “uneconomic assets”. I decided that this was the perfect time to buy Exelon and get the SpinCo assets on the cheap -

Aftermath

And then you had to just wait for the pendulum to start swinging in the other direction. It only got better after this point including support for existing Nuclear Power Plants in the Inflation Reduction Act of 2022. A Production Tax Credit of 0.3 cents/kWh is provided which rises to 1.5 cents/kWh for prevailing wage compliance. This can turn a shutdown candidate into a viable asset. Several states also provided their own Zero Emissions Credits, and this portion of the IRA survived the next admin except for some foreign-entity exclusions.

While PJM still has issues, reforms in 2024 changed how PJM measures capacity contributions and reliability risk. The idea is to better account for whether resources actually perform during high-risk hours, including winter stress and correlated outages.

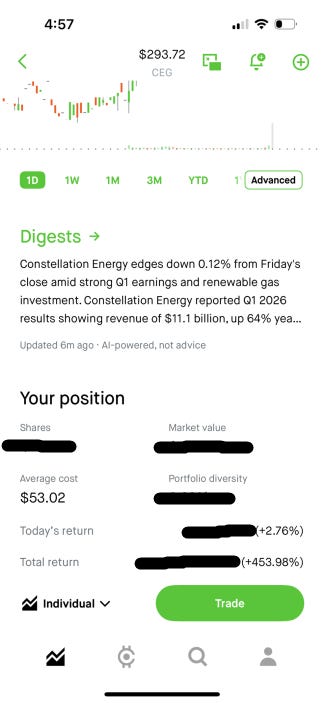

The Exelon generating arm SpinCo eventually became Constellation Energy CEG 0.00%↑ which holders of Exelon got one share for every three. As we all know, the biggest change has been that power is no longer in surplus due the AI driven demand and Hyperscalers’ willingness to pay directly for guaranteed 24/7 reliable low carbon power. The most famous example is of course Microsoft paying Constellation Energy to restart Unit 1 of the Three Mile Island nuclear plant pictured at the start of this article. Unit 2 has been dormant since the infamous core meltdown accident in 1979. Unit 1 was shut down in 2019 as uneconomic before the pending revival as part of this deal.

Closing thoughts

The shares I received as part of the spinoff are now more than a 5 bagger (I don’t think Robinhood calculated spinoff cost basis correctly but that’s a different issue that I need to take up with them) -

BTW that return beats even the return of SMH 0.00%↑ during the same period of time. Needless to say, I sold the original Exelon shares.

Finally, I will leave you with this quote -

“I made a lot of money in General Public Utilities, the owner of Three Mile Island. Anybody could have. You just had to be patient, keep up with the news, and read it with dispassion.”

— Peter Lynch | One Up on Wall Street

Still true today under different circumstances. I’ll bet that Lynch himself would be amused and surprised that you could make money once again buying the owner of Three Mile Island!

Disclaimer: None of this is meant as advice. I would encourage you to do your own research and invest according to your circumstances.